Financing products

When a company starts running out of cash, it rarely stops paying obligations randomly.

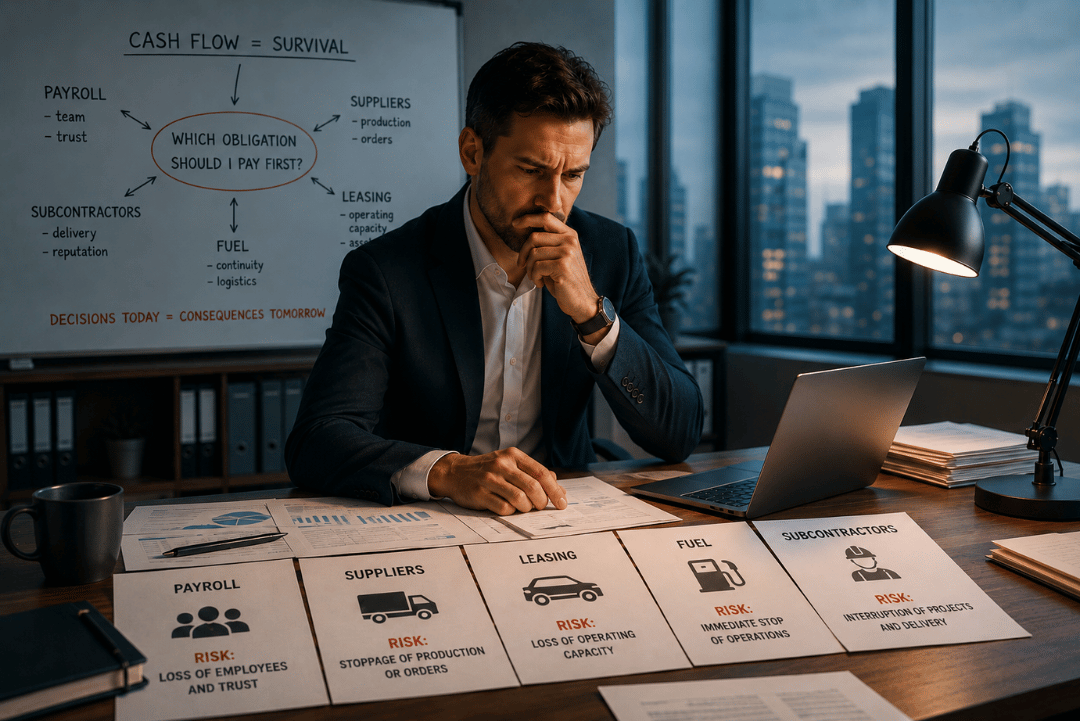

First, it protects the things that keep the business operating: salaries, suppliers, fuel, leasing, inventory, subcontractors, and contract execution costs. Only later, often as one of the last pieces of the puzzle, comes the decision to delay ZUS or tax payments.

That does not mean entrepreneurs consider these obligations unimportant. In fact, it reveals something far more concerning: for many businesses, ZUS and tax authorities become the last liquidity buffer.

As reported by 300Gospodarka, based on the “Financial Culture of Poles” study prepared for BIG InfoMonitor, companies struggling with liquidity most often postpone payments to public institutions. ZUS ranked first among the entities toward which businesses declared the highest willingness to delay payments. (300gospodarka.pl)

This is an important signal, because delayed ZUS payments are rarely the beginning of the problem. Much more often, they are the moment when earlier tensions become visible: a client paid too late, costs grew faster than margins, several obligations accumulated in the same week, and the company had to decide which payment to prioritize.

And that is why the real question is not simply: why do companies delay ZUS and tax payments? The better question is: what happens earlier, before a company starts treating them as a way to buy time?

ZUS and taxes become “the payment that can wait a little longer”

In theory, every obligation has a due date and consequences. In practice, an entrepreneur operating under liquidity pressure starts thinking differently: which delay would stop the business today, and which one would create problems slightly later? If salaries are not paid, the company risks losing people and team trust. If a key supplier is not paid, production or order fulfillment may stop. If leasing, fuel, or subcontractors are not covered, operations may quickly come to a halt.

ZUS and taxes, despite their very real consequences, are often viewed differently. They still give the company a little more time. And that is exactly why they become the last liquidity buffer for many businesses. Of course, this does not solve the problem. Quite the opposite - it often makes it worse. But it clearly shows the logic businesses follow during periods of financial pressure. Entrepreneurs are often not choosing between “paying or not paying.”

They are choosing between:

- keeping the business running today,

- and risking administrative and financial consequences several weeks later.

Delayed ZUS payments are rarely the beginning of the problem. More often, they are a symptom

Debt toward ZUS or the Tax Office rarely appears as the first warning sign of financial trouble. Usually, the company has already been operating for some time with a shrinking safety margin. Clients started paying later. Costs increased faster than expected. Contract margins turned out lower than planned. Several large payments accumulated at the same time. The company began financing one project with incoming cash from another.

From the outside, the business may still look stable. Sales exist. Clients exist. Projects continue. But internally, more and more energy starts being spent not on growth, but on managing the timing of cash flow. And that is why the question “why didn’t the company pay ZUS?” is often asked too late.

The more important questions are:

- when did the company begin losing control over its cash flow,

- why was the pressure noticed so late,

- and whether the problem comes from a temporary liquidity gap or a deeper weakness in the business model.

We discussed this mechanism further in our article about when debt toward ZUS and the Tax Office begins creating a debt spiral, and when financing can realistically help restore control.

The problem for many companies does not start with a lack of sales

This is one of the most important, and at the same time most misleading, aspects of liquidity problems. A company may have clients, revenue, and new contracts while still experiencing increasing cash pressure. That happens because sales and liquidity are not the same thing. Money may return too slowly compared to costs. A company may need to finance contract execution long before receiving payment itself. Several larger expenses may accumulate within the same week. Delayed client payments can start creating a domino effect.

And that is the moment when entrepreneurs begin managing payment priorities instead of truly controlling cash flow. That is why many businesses struggling with liquidity do not look like companies “in crisis.” They are often growing businesses with assets and active operations.

The real issue is that costs begin requiring cash faster than the company can recover it. We explore this further in our article about the difference between cash flow and profit.

The biggest risk? The company buys time, but loses room to maneuver

Delaying ZUS or tax payments often provides temporary relief. It allows the company to pay employees. Keep suppliers. Deliver contracts. Avoid stopping operations at the worst possible moment. The problem is that this relief is usually very short-lived.

Public debt obligations begin generating interest, stress, enforcement risk, and increasing operational pressure. They may also complicate conversations with banks, leasing companies, or financing institutions, because overdue payments toward ZUS and the Tax Office are among the first warning signs analyzed during risk assessments. And that is why financing public liabilities only makes sense when it becomes part of stabilizing the situation, not another attempt to postpone the problem.

What is needed is:

- a realistic repayment source,

- regained control over cash flow,

- understanding the root cause of the issue,

- and a plan that prevents the same mechanism from repeating in a few months.

We discussed this further in our article about when non-bank financing for businesses actually makes sense, and when it simply increases risk.

The problem for many companies is not a lack of data. The problem is seeing it too late

In many cases, entrepreneurs only realize there is a problem when they must decide:

- whether to pay ZUS,

- salaries,

- leasing,

- or suppliers.

That means visibility failed earlier. The company did not notice soon enough that several large payments would accumulate at the same time. It did not see that contractors were gradually extending payment terms. It lacked a full picture of costs and liabilities for the coming weeks.

And that is why the importance of business management today goes beyond sales alone. Increasingly, companies need:

- real-time visibility into costs,

- faster document workflows,

- liability control,

- better understanding of cash flow,

- earlier detection of liquidity pressure.

That is also why more and more businesses are automating financial processes and moving away from fragmented Excel files and email-based workflows. We discussed this further in the articles Is Your Excel Lying to You? and OCR vs Manual Invoice Entry.

ZUS should not become an early warning system

If a company only realizes it has a liquidity problem once it starts delaying ZUS or tax payments, it means the warning signs appeared far too late. Because real liquidity control does not begin with the question: “Which payment can we still delay?”

It starts much earlier:

- with predicting liquidity pressure,

- understanding costs,

- controlling cash flow,

- and seeing what will happen in one week, two weeks, or a month.

ZUS and tax liabilities often become simply the moment when an earlier problem stops being invisible.